A record build pressures LCFS prices. Available to read at and property of ArgusMedia.com.

A second consecutive record build in California Low Carbon Fuel Standard (LCFS) credits added pressure to spot and forward markets today.

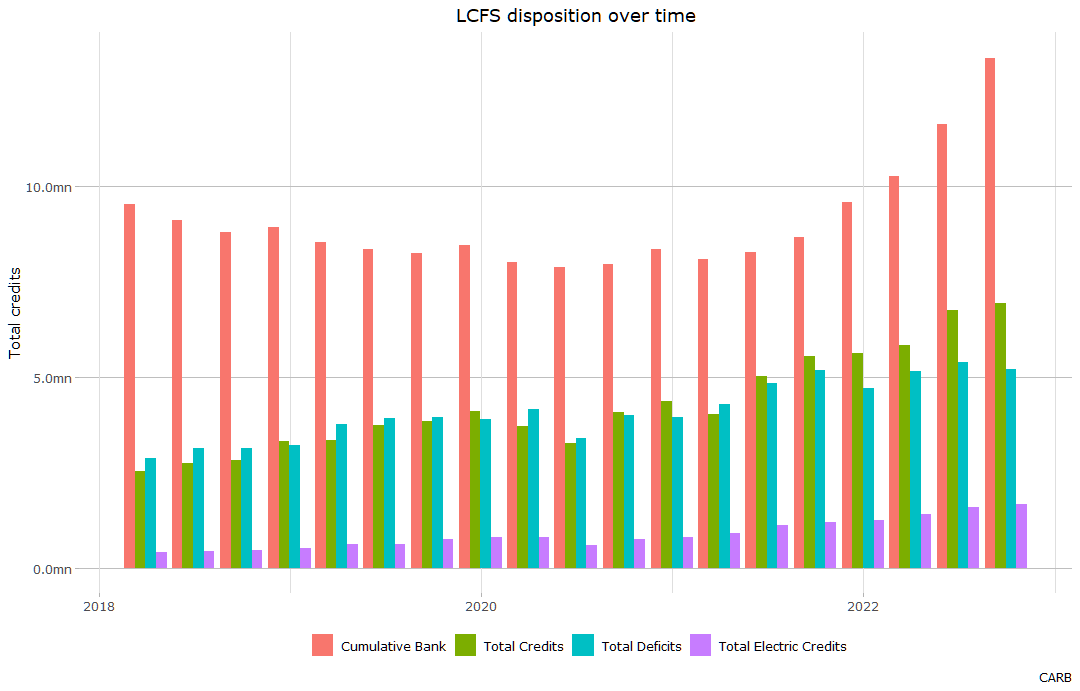

New LCFS credits outpaced program deficits by a record 1.7mn metric tonnes (t) in the third quarter of 2022, building unused credits available for compliance to 13.4mn t, according to California Air Resources Board (CARB) data released today.

New credits have exceeded deficits for six consecutive quarters, and posted new record increases for the past two. The rising volume of credits that can be used to comply with state mandates and do not expire have raised alarms from renewable fuel producers seeking tougher new standards for one of the top low-carbon fuel markets.

LCFS programs require yearly reductions in transportation fuel carbon intensity. Conventional, higher-carbon fuels that exceed the annual limit incur deficits that suppliers must offset with credits generated from the supply of approved, low-carbon alternatives.

Rising supplies of these low-carbon fuels have met sluggish demand for California’s gasoline blendstock and largest LCFS deficit source, CARBOB. The fuel still generated 79pc of all new deficits during the third quarter, even as overall consumption fell by 3.1pc from the previous quarter and by 8.5pc from the third quarter of 2021. Petroleum diesel consumption fell by 29pc from the third quarter of 2021.

Deficits generated from the consumption of petroleum gasoline and diesel in the state fell by 3.5pc from the previous quarter as demand for both shrank during the period.

Credit generation meanwhile continued to climb, up by 2.7pc from the previous quarter, as renewable natural gas, ethanol and electric vehicle charging all produced more credits than in the previous quarter.

Renewable diesel credits meanwhile shrank, as smaller volumes of higher-carbon production found their way to the state during the quarter. Both used-cooking oil- and tallow-based renewable diesel consumption exceeded volumes in the third quarter of 2021 but fell by a combined 22pc from the previous quarter. Corn oil-based renewable diesel increased sharply. Renewable diesel remained the leading source of new credits, at 39pc of all generated during the third quarter of 2022.

Lower, longer

California LCFS credit prices have groaned under the weight of record supplies. Credits do not expire, and so parties may use the growing bank of untapped credits to meet current and future obligations.

Spot credits that traded around $200/t in January 2021 slumped to a six-year low in September 2022, near $60/t. Spot credits have traded between $60-70/t since then, even as CARB reported the previous 11.3mn t record volume of unused credits at the end of October.

Credits immediately sank following the data release early in the second half of today’s trading session. Bids for prompt through second quarter 2023 credit transfers briefly dipped to $58/t.

Renewable fuel suppliers have clamored for CARB to respond to the rising unused credit volume with tougher targets. CARB staff have said that a rulemaking to consider revisions to the LCFS would begin early this year.

By Elliott Blackburn